$150,000 instant asset write-off threshold to be extended to 31 December 2020

On 12 March 2020, the instant asset write-off (IAWO) measure was extended so that for the period between 12 March 2020 and 30 June 2020 IAWO became available for assets costing less than $150,000 (subject to certain restrictions such as the car cost limit). Additionally, eligibility was expanded from businesses with aggregated annual turnovers below $10m to businesses with aggregated annual turnovers below $500m.

This concession was legislated to run to 30 June 2020 and from 1 July 2020 the IAWO was to revert to the $1,000 asset cost limit with the eligibility turnover threshold to revert to below $10m.

In a welcome development, the Treasurer announced on 9 June that the 30 June 2020 end date for the extended IAWO will be pushed out to 31 December 2020. This provides businesses with another 6 months to take advantage of the current generous IAWO rules and invest in eligible business assets in a tax-effective manner. We expect that this announcement will soon be followed by legislation to give businesses confidence in planning and undertaking major purchasing decisions as at this stage it is only an announcement.

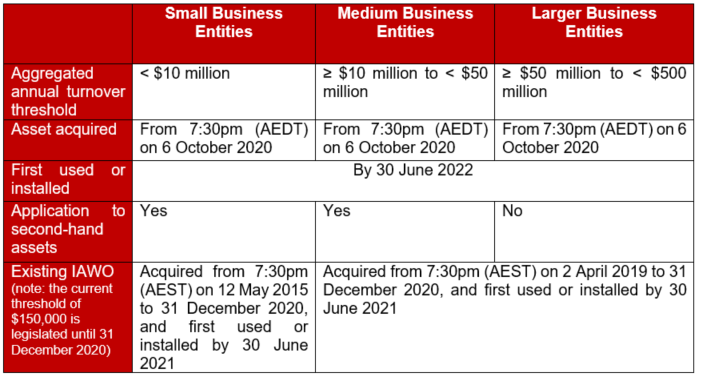

In addition to IAWO, the accelerated 50% depreciation measure will continue to be available until 30 June 2021. This summary shows the depreciation concessions available to businesses:

We encourage you to review our Depreciation Concessions article in our COVID-19 Info Hub where we have provided additional guidance on how the IAWO and the accelerated 50% depreciation measures apply in practice, and on their interaction with the car cost limit.

As always, we are here for you to answer any questions you may have about the tax concessions available to your business including the depreciation measures discussed here. We encourage you to get in touch with your Ruddicks adviser if you need any further information.

DISCLAIMER:

Liability limited by a scheme approved under Professional Standards Legislation.

The content of this newsletter is general in nature. It does not constitute specific advice and readers are encouraged to consult their Ruddicks adviser on any matters of interest. Ruddicks accepts no liability for errors or omissions, or for any loss or damage suffered as a result of any person acting without such advice. This information is current as at 10 June 2020, and was published around that time. Ruddicks particularly accepts no obligation or responsibility for updating this publication for events, including changes to the law, the Australian Taxation Office’s interpretation of the law, or Government announcements arising after that time.

Any advice provided is not ‘financial product advice’ as defined by the Corporations Act. Ruddicks is not licensed to provide financial product advice and taxation is only one of the matters that you need to consider when making a decision on a financial product. You should consider seeking advice from an Australian Financial Services licensee before making any decisions in relation to a financial product. © Ruddicks 2020