Super Guarantee Increase

Whilst the increases have been in place legislatively for some time, there was a wide expectation that the first increase to 10% this July would be frozen once again. Plenty of debate between the political parties and views put forward by the big industry funds has occurred and after many months of contemplating the issue, the Federal government has decided against making any adjustments to the increases.

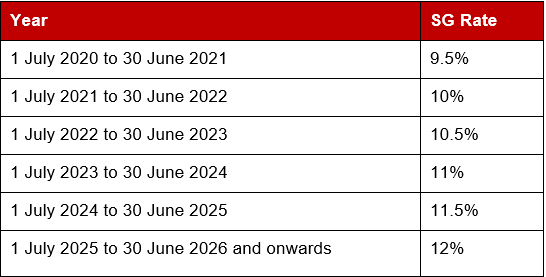

The Superannuation guarantee (SG) is legislated to increase as follows:

In preparation for the change, there are a series of important considerations and reviews that should be undertaken. Consider the following:

- Employment contracts should be reviewed – are employees salaries recorded as a package including super or as salary plus super? Will the employer incur the extra 0.5% SG or will the employee absorb this with lower take home pay? Could you consider timing or bringing forward any scheduled salary increases to 1 July 2021 to assist employees who will get lower take home pay because of the SG increase? Do you need to check and refer to any Awards or Workplace Agreements?

- For any changes and decisions that are made on this by employers – they should be clearly communicated with staff. Employers should be transparent and prepared to have discussions where necessary.

- Are your payroll systems ready for this change from 1 July 2021? Upgrades may be necessary. It’s a good opportunity to review whether you have all the appropriate details for each employee and their super fund in your payroll.

Some key notes regarding the Superannuation Guarantee are:

- The SG is payable to employees who get paid $450 or more per month (before tax).

- The May Budget announced a change to remove this threshold, which is expected to apply from 1 July 2022. From that date there will be no threshold on when SG applies to employees.

- SG is based on an employee’s “ordinary times earnings” (overtime pay for example is not included) and is due 28 days after the end of each quarter.

- If payment is not made by this date, then the employer must pay the Superannuation Guarantee Charge, which incorporates a penalty for late payment. Crucially, the base for SG charge is broader than ordinary times earnings, which can further increase the employer’s payment for being late.

- For the year commencing 1 July 2021, the maximum super contributions base will increase to $58,920 per financial quarter or $235,680 per year (which equates to maximum required superannuation contributions of $5,892 per quarter or $23,568 per year). This means the employer is not necessarily obligated to pay SG to employees on the portion of their salary above the maximum amount of $235,680 per year. Ultimately though it will be dependent on the employment contract and the terms agreed between employer and employee.

- Salary sacrificed contributions do not count towards the SG. The 10% needs to be based on an employee’s ordinary times earnings before any salary sacrifice superannuation amounts are deducted.

- From 1 July 2021, the annual concessional contributions cap will rise to $27,500 (it is currently $25,000 for the year ending 30 June 2021). This could be relevant for employees in considering their salary packaging arrangements going forward. It could also be useful for employees who receive superannuation on salary in excess of the maximum super contributions base.

It is the employer’s obligation to ensure employees are not underpaid their SG entitlement, otherwise you risk your business being subject to penalties under the SG Charge mentioned above.

The ATO has not indicated that it will give any leniency or grace period to employers who don’t meet this new SG obligation so it is key to be prepared and ready for these changes when they come on July 1 2021.

Should any of our clients have any questions or concerns regarding these changes, please do not hesitate to contact our office and we will be happy to assist you in any way we can.

DISCLAIMER:

Liability limited by a scheme approved under Professional Standards Legislation.

The content of this newsletter is general in nature. It does not constitute specific advice and readers are encouraged to consult their Ruddicks adviser on any matters of interest. Ruddicks accepts no liability for errors or omissions, or for any loss or damage suffered as a result of any person acting without such advice. This information is current as at 17 June 2021 and was published around that time. Ruddicks particularly accepts no obligation or responsibility for updating this publication for events, including changes to the law, the Australian Taxation Office’s interpretation of the law, or Government announcements arising after that time.

Any advice provided is not ‘financial product advice’ as defined by the Corporations Act. Ruddicks is not licensed to provide financial product advice and taxation is only one of the matters that you need to consider when making a decision on a financial product. You should consider seeking advice from an Australian Financial Services licensee before making any decisions in relation to a financial product. © Ruddicks 2021