Superannuation Bulletin

Under the new rules, broadly, people with pension balances above $1.6m will pay more tax on investment earnings (albeit at the concessional 15% tax rate) and the opportunities to make superannuation contributions will be reduced, with lower contribution caps to apply from 1 July 2017.

It must be emphasised that these changes are remarkably complex and represent the most significant overhaul of the superannuation system since 2007. With complexity comes risk that inadvertent breaches may lead to non-compliance with superannuation rules and subsequent penalties. Any superannuation advice would need to be given on a case by case basis taking into account individual circumstances and important decisions have to be made by SMSF Trustees by 30 June 2017.

Accumulation Phase

This section is relevant to super fund members who are still contributing to superannuation, including via mandated employer contributions at 9.5%.

Concessional cap

Note: concessional contributions include superannuation guarantee contributions from your employer, salary sacrificed amounts and personal contributions for which you claim a tax deduction in your personal tax return.

From 1 July 2017:

- The concessional contribution cap will be reduced from $30,000 for those under age 50 and $35,000 for ages 50 and over, to a single cap of $25,000 irrespective of age. The new cap will be indexed to average weekly ordinary time earnings in $2,500 increments.

- All individuals up to age 65, and those aged 65 to 75 who meet the work test (i.e. those who undertake at least 40 hours of paid employment within a 30 day period), will be able to claim an income tax deduction for personal superannuation contributions. Previously, the 10% test applied to limit tax deductions to those who derived no more than 10% of their income from employment-related activities. The 10% test will be scrapped going forward, allowing individuals to top up their super and claim tax deductions for contributions in their own tax returns.

Our commentary:

This a great development opening up tax deductible super contributions to a wide range of people previously ineligible, such as employees.

WARNING: total concessional contributions will be subject to the annual $25,000 cap, which will also include the 9.5% superannuation guarantee contributions and any salary sacrificed amounts!

If you are currently salary sacrificing into super to the maximum limit, you should consider reviewing your arrangements prior to 30 June 2017, taking into account the reduced contribution limit for the 2017/18 year.

- From 1 July 2012, an additional tax of up to 15% (known as Division 293 tax) has been payable by high income earners in respect of their concessional superannuation contributions. From 1 July 2017, the threshold from which Division 293 tax applies will be lowered from $300,000 to $250,000. This means that individuals with personal adjusted taxable incomes of $250,000 and above will be paying tax of up to 30% on their concessional contributions, while everyone else will continue paying just 15%.

Our commentary:

Whilst this will make concessional contributions to super for some high income earners less tax effective, superannuation remains a highly attractive wealth creation vehicle for most people.

From 1 July 2018

- Individuals with total superannuation balances under $500,000 will be able to carry forward their unused concessional cap balances for 5 years on a rolling basis. This will allow catch-up contributions to be made where an individual's concessional caps have not been fully used up in previous years, however only unused amounts accrued from 1 July 2018 onwards can be carried forward.

- For example, an investor with no employer contributions who does not use the concessional contribution cap for 4 years (e.g. 2019 to 2022), will be able to make a personal concessional contribution of up to $125,000 in the fifth year, 2023 ($25,000 x 5). This can particularly help with tax planning in the years when a spike in taxable income is expected, such as from the sale of an asset with a capital gain.

Non-concessional cap

Note: non-concessional contributions are personal after-tax contributions made by individuals under age 65 and those aged 65 to 75 who meet the work test (i.e. those who undertake at least 40 hours of paid employment within a 30 day period), with their own funds for which a tax deduction is not claimed in your personal tax return.

Unlike concessional contributions, the main benefit for making non-concessional contributions is not any immediate tax benefit, but rather the transfer of funds into the low tax superannuation environment.

From 1 July 2017:

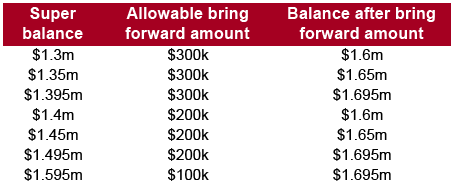

- The non-concessional contribution cap has been lowered from $180,000 to $100,000 per year with the new cap indexed to average weekly ordinary time earnings in $2,500 increments. The three year bring-forward rule will continue to be available for individuals under 65 and whose total superannuation balance is below $1.6m. This includes both pension and accumulation accounts in all superannuation funds you are a member of. For those individuals who have triggered the three year bring-forward rule in the 2016 or 2017 financial years, the remaining amounts that can be contributed will be adjusted as follows:

- If your total superannuation balance at 30 June is over $1.6m, then you will not be permitted to make further non-concessional contributions in the subsequent year.

- If your total superannuation balance is close to $1.6m, then you will only be able to contribute (and use the bring-forward rule) in $100,000 increments while you are under $1.6m. This means that people with a superannuation balance close to $1.6m will need to be very careful before making non-concessional contributions to ensure that they do not breach the new rules.

- For example, an individual with a superannuation balance of $1.45m on 30 June 2017 can make non-concessional contributions of no more than $200,000 in the 2018 financial year, using the bring-forward rule. This person would not be able to access the full 3 year bring forward of $300,000 as this would take the superannuation balance over $1.6m. The table below demonstrates the interaction of the non-concessional contribution rules with the new $1.6m total superannuation balance cap.

If you breach the cap by contributing too much, the excess will have to be taken out, with deemed earnings on the excess taxed at the standard 15% fund rate for a first time cap breach and at 30% for subsequent breaches. The earnings are currently deemed at 8.76% (calculated as the 90 day bank bill rate plus 7%).

IMPORTANT - KNOW YOUR CAPS!

The new $1.6m total superannuation balance cap is different from the $1.6m pension account cap (officially referred to as the balance transfer cap) which is discussed below. The $1.6m total superannuation balance cap is one of the factors that determine your ability to make non-concessional contributions. It includes all your superannuation balances, across all superannuation funds you are a member of.

The $1.6m balance transfer cap is effectively a cap on how much of your superannuation money can be put into the tax-free pension phase. It only includes the sum of all pension accounts you have, across all superannuation funds you are a member of. Accumulation accounts do not count towards this cap.

Our commentary:

The implication of the reduction in the annual non-concessional contribution limit from $180,000 to $100,000, and the new exclusion from making non-concessional contributions for those with super balances of over $1.6m, is clear: you have until 30 June 2017 to take advantage of the existing, significantly more generous non-concessional contribution rules.

You should act now, before this window closes, and discuss your specific circumstances with us at your earliest opportunity.

Low income super contribution

- The current Low Income Superannuation Contribution rules will be replaced by Low Income Superannuation Tax Offset (LISTO), which will provide a non-refundable tax offset to super funds of up to $500, to offset tax payable on concessional contributions made on behalf of members with adjusted taxable incomes of up to $37,000.

- Access will be increased to the low income spouse superannuation tax offset by raising the income threshold for the low income spouse from $10,800 to $37,000. The offset provides up to $540 per year for the contributing spouse.

Pension Phase

This section is relevant to super fund members who meet one or more conditions of release and who are eligible to make withdrawals from their superannuation balances.

From 1 July 2017:

Transition to Retirement Income Stream/Pension (TRIS)

- A TRIS is generally a pension received by someone under age 65 who has not satisfied the ‘retirement’ condition of release at some point after their preservation age.

- Earnings in respect of assets supporting TRIS pensions will no longer be tax-free, with the standard super fund 15% tax rate applying from 1 July 2017 (10% for discount capital gains).

- Additionally, the rule that currently allows individuals to treat certain pension payments as lump sums for tax purposes will be removed. The lump sum treatment allows withdrawal of funds to be tax-free in the hands of the recipient, up to the lifetime low rate cap amount (currently $195,000). This opportunity will still exist up to 30 June 2017.

- CGT relief, explained below, will also be available to TRIS recipients to shelter the capital gains on assets supporting the TRIS which have accrued up to 30 June 2017. This will secure the 0% tax rate for those capital gains, while the gains accrued after that date will be subject to the 10% tax rate for discount gains.

- If you are unsure if your pension is a TRIS, please contact your Ruddicks adviser to discuss your circumstances and the effect this change may have for you.

Our commentary:

Super fund members under age 65 currently in receipt of a TRIS should give consideration to “retiring” on or before 30 June 2017 in order to preserve the tax-free status of the super fund’s income. The concept of “retirement” has specific definitions within the tax law and we would be happy to discuss this with you, as well as to quantify the possible tax benefits of retirement for your personal circumstances.

If you can't satisfy the "retirement" criteria, you will need to consider whether to continue any existing TRISs beyond 30 June 2017, when most of the tax benefits will cease.

Pension account cap

- A $1.6 million ‘balance transfer cap’ will apply from 1 July 2017 on the amount of superannuation an individual can transfer from the accumulation phase to the pension phase. This means that earnings in respect of assets supporting a pension balance (excluding TRISs) of up to $1.6m will remain tax exempt to the fund, while earnings on assets in excess of $1.6m per person will be taxed at the standard 15% fund tax rate applicable to accumulation monies, with discount capital gains taxed at 10%.

- The value of pension accounts as at 30 June 2017 will count towards the cap, as well as the value of pension accounts commenced from 1 July 2017 onwards. Additionally, the value of reversionary pensions will count towards the recipient’s cap, although there is a 12 month exemption after the death of the original pension recipient to allow for restructuring.

- Investment gains and losses, and annual pension drawings will not be counted towards the cap. As a result, the pension account may grow above $1.6m by virtue of investment earnings without penalty.

- If at 30 June 2017 your pension accounts in total exceed the $1.6m cap, the excess will need to be reallocated to an accumulation account. For members meeting this limit in SMSFs, this will likely result in some additional once-off legal paperwork and costs to comply with this requirement.

- The cap will be indexed in line with CPI movements in $100,000 increments.

Our commentary:

This change will result in additional tax being payable by super fund members with balances over $1.6m currently paying pensions. These members will be subject to an average rate of tax on the super fund’s income of somewhere between 0% and 15%, depending on the balance of the fund, from 1 July 2017. While this will be higher than the current 0% rate, the income of super funds will remain very concessionally taxed.

Previously, best practice was usually to get as much money as possible into a member’s super fund. From 1 July 2017, some members may be better off withdrawing some funds from superannuation and investing them in their own name, especially where they have minimal other income. We would be happy to look at your specific circumstances and discuss whether this might be appropriate for you.

CGT Relief

- The introduction of the $1.6m balance transfer cap will require some people to unwind existing pension arrangements to reallocate assets in excess of $1.6m out of the pension environment and into accumulation. When those assets are ultimately sold, the capital gain would be taxable to the fund. In a welcome surprise, under the new rules, capital gains tax (‘CGT’) relief is available on an opt-in basis to exempt any capital gain accrued up to 30 June 2017.

- The relief would operate as a deemed disposal and reacquisition of assets on 30 June 2017 therefore making it necessary to be in a position to determine market value of relevant assets at that date, especially unlisted assets such as real estate, where values may not be readily available.

- Where a CGT relief election is made, the 12 month period for the purposes of the CGT discount will restart on 1 July 2017, meaning that if the asset which previously supported a pension account is sold before 1 July 2018, any capital gain accrued since 1 July 2017 will not be subject to the 33% CGT discount. This means that effectively non-discount gains are taxed at 15% compared to 10% for discount gains. In some instances, a better outcome may arise if the CGT relief is not chosen.

- The CGT relief provisions are particularly complex, requiring an asset by asset analysis and written elections within prescribed time limits. We strongly suggest that you consult with your Ruddicks adviser if you are affected by the $1.6m cap in order to determine the best approach in your circumstances. For those SMSFs that Ruddicks administer, we will proactively work through this process with you.

Unchanged

Capital drawdowns by way of a pension or lump sum on or after age 60 will continue to be tax exempt in the hands of the individuals.

Planning ahead

Should I sell the assets in my SMSF before 30 June 2017 to take advantage of the 0% tax rate and crystallise any accrued gains?

In most circumstances, the CGT relief provisions will achieve the same outcome without incurring transaction costs, although the complexity of the provisions may lead some SMSF trustees to sell the assets as an easier approach.

Warning! Unless using the CGT relief provisions, selling and repurchasing identical assets in close succession can trigger tax avoidance rules! Please consult us before taking this approach.

Is it still tax effective to keep my money in superannuation?

Superannuation funds remain tax effective structures, with a maximum tax rate of 15%, compared to 27.5% or 30% for companies (depending on whether they are carrying on a business), or personal marginal tax rates of up to 49% including Medicare Levy. In most instances, it would be beneficial to keep your money in the superannuation environment rather than taking it out (although your personal circumstances should be taken into account).

Is there a tax benefit to opening another super fund to separate my pension and non-pension assets?

From the tax perspective, it may be easier to access the 0% tax rate on earnings by separating the pension assets of up to $1.6m in another superannuation fund, however there are other considerations involved in making this decision, such as the increased operating costs and we suggest you discuss your circumstances with us and your financial adviser.

Is there anything I can do to minimise the tax impact of the new pension account cap if my super balance is likely to end up above the $1.6m cap but my spouse’s is well below the cap?

It may be best to even up the superannuation balance between spouses where one is at risk of breaching the $1.6m cap. This can be achieved by strategic allocation of non-concessional contributions to the account of the spouse with the lower balance, as well as by splitting of concessional contributions. Please contact us to discuss these options.

IMPORTANT! What to do now to prepare for the new rules coming into effect

- If you have a TRIS, or think you might do, contact us to discuss the tax implications for your TRIS after 1 July 2017.

- If you are thinking about putting more money into superannuation via contributions, be mindful of the changes to contribution caps and the reduced bring-forward cap for non-concessional contributions. Please discuss with your Ruddicks adviser if you are contemplating making significant contributions or are unsure about the status of your contribution caps.

- If your superannuation balances are in excess of $1.6m, please contact us to discuss the approach to unwind the excess funds and the availability of the CGT relief. Be prepared to obtain valuations of unlisted investments held within your fund as at 30 June 2017.

The new rules significantly change the taxation of superannuation and there is a need for increased vigilance when making any significant decisions and transactions relating to superannuation. Overall, the reduced contribution caps will be the most significant change for most people, while those with close to, or more than, $1.6m in superannuation will be required to make important tax elections by 30 June 2017.

The changes also mean that the 2017 financial year may be the last opportunity to take advantage of the current rules and we encourage our clients to contact their Ruddicks advisers to discuss the issues raised in this bulletin.

Disclaimer

The information and opinions in this article were prepared by Ruddicks Chartered Accountants (“Ruddicks”) for general information purposes only.

Taxation is only one of the matters that must be considered when making a decision on a financial product. The taxation considerations discussed in this article are based on the continuation of the present laws and their interpretation. The tax consequences of any investment will depend on individual circumstances.

In preparing this article Ruddicks have not taken into account the investment objectives, financial situation and particular needs of any particular investor. The information contained herein does not constitute advice nor the promotion of any particular course of action or strategy and you should not rely on any material in this article to make (or refrain from making) any decision or take (or refrain from taking) any action.

Ruddicks are not licensed to give financial product advice under the Corporations Law. You should consider taking advice from an Australian Financial Services Licensee before making a decision on a financial product such as superannuation.

Opinions, estimates and projections in this article constitute judgement of Ruddicks as of the date of this publication and are subject to change without notice. Ruddicks have no obligation to update, modify or amend this article or to otherwise notify a reader thereof in the event that any matter stated herein, or any opinion, projection, forecast, estimate set forth herein, changes or subsequently becomes inaccurate.

Ruddicks believe that the information contained in this document is accurate when issued. Ruddicks do not warrant that such information is accurate, reliable, complete or up to date, and, to the fullest extent permitted by law, disclaim all liability of Ruddicks, its officers, employees, agents and associates (“Associates”) for any loss or damage suffered by any person by reason of the use by that person of, or their reliance on, any information contained in this document or any error or defect in this document, whether arising from the negligence of Ruddicks or its Associates or otherwise.

This article may not be reproduced, distributed or published by any person for any purpose without Ruddicks’ prior written consent. Enquiries should be addressed to Ruddicks Chartered Accountants. © Ruddicks 2016